Supply Chain Uncertainty, Energy Prices, and Inflation

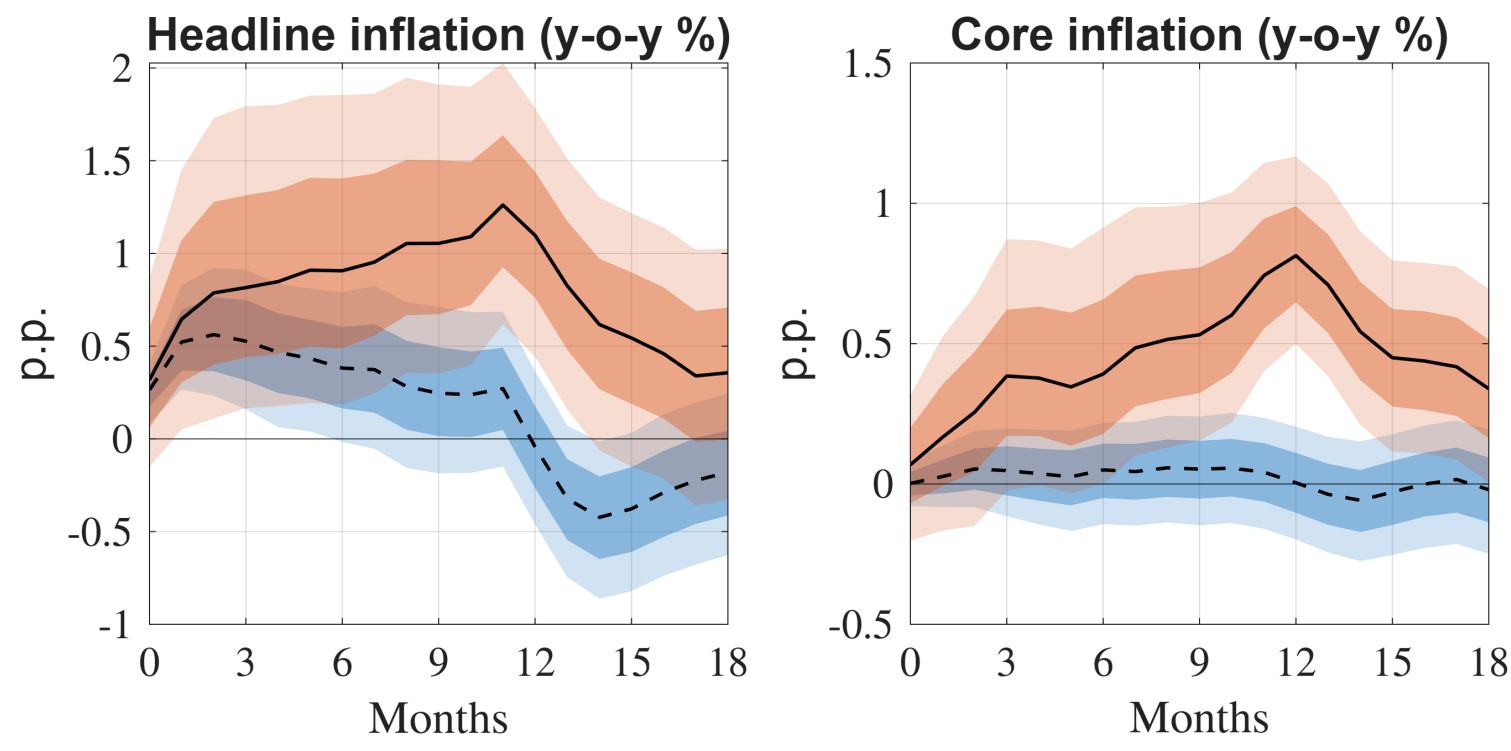

Abstract. Using U.S. and Euro area data, we document that (i) the pass-through of energy prices to inflation is state-dependent - stronger when supply chain uncertainty is elevated - and (ii) in such states, energy prices become more informative about logistical conditions. We develop a model in which firms combine energy and a specialized input transported through a capacity-constrained transportation network. When congestion binds, energy remains available in local markets at a premium, whereas the specialized input is subject to delivery delays. Because energy prices reflect both raw energy shocks and transportation conditions, firms treat them as noisy signals of supply disruptions and update beliefs through Bayesian learning. This signal-extraction channel increases perceived marginal costs, generating an uncertainty wedge that amplifies and propagates energy shocks. Within a general-equilibrium New Keynesian model, the mechanism raises the impact elasticity and the persistence of inflation in response to transitory energy shocks. This challenges the conventional monetary policy prescription to “look through” supply disturbances. ...